What are ground-mounted solar power systems?

And when will a solar farm pay for itself in 2026?

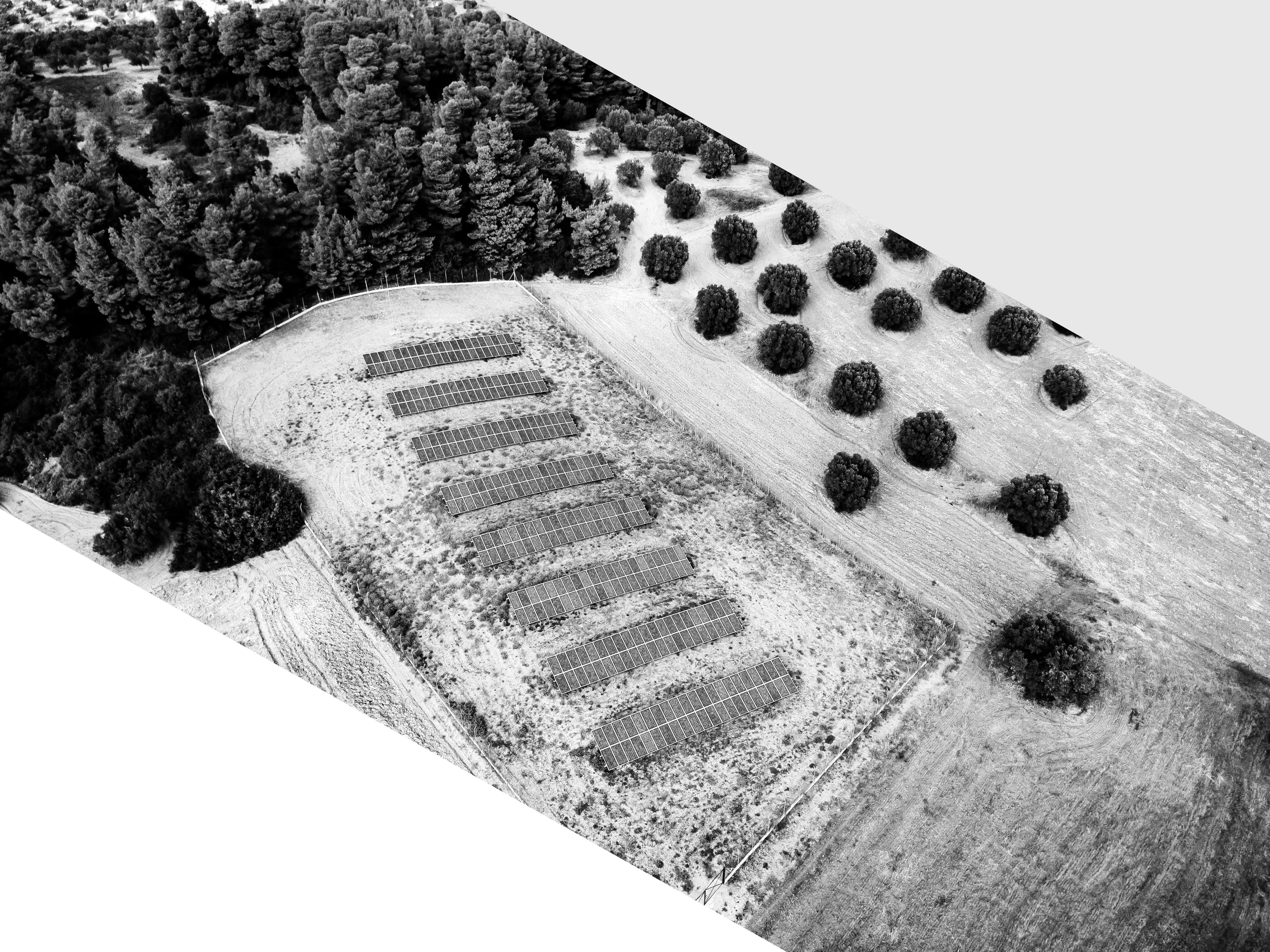

A ground-mounted photovoltaic system (abbreviated as PV FFA or ground-mounted PV system) is a ground-mounted solar system typically ranging from 750 kWp to over 600 MWp. Ground-mounted photovoltaic plants require approximately 1.0 ha per MWp, are ideally located within a 200-meter strip along a highway or railway line (§ 35 BauGB), and will achieve a maximum bid price of 5.79 ct/kWh in the 2026 tenders (BNetzA, bid deadline March 1, 2026). Landowners receive a lease of €2,500–4,500/ha/year for their land. The investment in ground-mounted solar plants is €600–900/kWp for projects over 10 MWp (Fraunhofer ISE / BSW Solar, Q1 2026).

Table of Contents

What distinguishes ground-mounted photovoltaic systems from rooftop and dual-use systems

Land requirements, location, and suitability—the key considerations for landowners

Capital costs and levelized cost of electricity for ground-mounted photovoltaic systems in 2026

Solar Farms as an Investment: Factors Driving Returns and Market Conditions

Biodiversity and the Ecological Benefits of Modern Solar Farms

By 2026, ground-mounted photovoltaic systems had become the most important pillar of Germany’s PV expansion. According to figures from the Federal Network Agency, approximately 8.2 GW of new ground-mounted photovoltaic capacity was installed in 2025—exceeding the total capacity of new rooftop photovoltaic systems (7.8 GW) for the first time. Commercial and industrial sectors benefit most from these rooftop photovoltaic systems, while ground-mounted photovoltaic systems dominate the large-scale megawatt tenders.

At the same time, the legal framework has changed significantly: Since January 11, 2023, the designated buffer zone along highways and railways has been set at 200 meters (Section 35(1)(8)(b) of the German Building Code (BauGB)). The Helm Group, comprising mediplan Helm e.K. and Logic Energy, has been supporting landowners, municipalities, and citizens for over 40 years with ground-mounted solar and PV systems—from site selection through to long-term operation—including projects ranging from 1 to 250 MWp. This article provides an overview of the key figures, laws, and opportunities relevant to decision-making for 2026, thereby making a factual contribution to the energy transition and climate protection. Among other topics, it covers leases, costs, permitting, and revenue in detail.

This article is intended for landowners, investors, local governments, and anyone interested in the development and economic viability of ground-mounted solar power plants.

What is a ground-mounted photovoltaic system—and how does it differ from other types?

A ground-mounted photovoltaic system (also known as a ground-mounted PV system, PV FFA, or FFA) is a ground-mounted facility for generating electricity on open land. Ground-mounted photovoltaic systems become economically viable at around 750 kWp and can scale up to large-scale projects such as the Witznitz Energy Park with 605 MWp (MoveOn Energy). Distinction: Unlike a dual-use system, the land is not used for agricultural purposes at the same time; unlike rooftop photovoltaic systems, no building structure is required.

Distinction from Roof, Floating, and Dual Use

A traditional ground-mounted photovoltaic system covers the entire area with solar modules and a support structure. The modules in ground-mounted photovoltaic systems are typically mounted on metal frames without concrete foundations, which allows for dismantling without leaving any residue at the end of the system’s lifespan. The abbreviations FFA and PV FFA have become standard in technical jargon; PV FFA, PV ground-mounted system, ground-mounted photovoltaics, and ground-mounted photovoltaic systems essentially refer to the same thing. Photovoltaic systems on roofs utilize the roof surfaces of existing buildings and do not compete for land or space availability—details are covered in the sub-pillar on commercial rooftop systems.

The dual use of land for agriculture and solar power generation is a field in its own right and is explored in greater depth in the sub-pillar on agri-photovoltaics. Floating PV systems are installed on disused quarry ponds or reservoirs and remain a niche segment in Germany. For areas of 3–4 hectares or more and for the exclusive generation of electricity, traditional ground-mounted solar systems—that is, ground-mounted solar systems in the narrower sense—are typically the most economical choice. The terms “PV FFA” and “FFA” are intentionally used interchangeably in the text so that readers can easily identify various spellings of “PV FFA.”

Typical project sizes for ground-mounted photovoltaic systems: 1 to 605 MWp

Ground-mounted photovoltaic systems vary widely in size. Ground-mounted photovoltaic systems can be operated profitably on sites of at least 20,000 square meters, which makes them particularly attractive to commercial investors. Community energy projects start at 1–6 MWp, standard EEG projects range between 10 and 50 MWp, and large-scale projects exceed 100 MWp. According to data from the Market Master Data Register, Germany currently operates around 21,700 solar parks with a combined capacity of approximately 40 GW (strom-report.com, as of 12/2025). The largest project is the Witznitz Energy Park in Saxony with 605 MWp and an expanded target of 650 MWp (MoveOn Energy, 04/2024). For landowners, municipalities, and citizens, project size is not merely a cosmetic consideration—it determines the type of grid connection, the permitting process, and the economic viability range.

How much land do ground-mounted solar power plants require—and which sites are suitable?

Modern ground-mounted photovoltaic systems require approximately 1.0 ha per MWp for south-facing installations and 0.7–0.8 ha per MWp for bifacial east-west mounting (C.A.R.M.E.N. e.V., 11/2025). Open-field photovoltaic systems become economically viable at 3–4 MWp on 4–5 ha. Under the Renewable Energy Act (EEG), eligible sites primarily include conversion areas, roadside strips up to 500 m along highways and railways, areas in disadvantaged regions, and impervious surfaces (Section 37(1)(2) EEG).

Rules of thumb for space requirements and space efficiency

Land requirements are the first figure every landowner needs to know. A 1-MWp south-facing ground-mounted PV system occupies about one hectare, including row spacing for maintenance aisles. With bifacial east-west trackers, up to 1.4 MWp/ha can be installed while using the same amount of land. The land efficiency of modern PV FFA is thus significantly higher than five years ago, because both modules and mounting structures have been further developed. A PV FFA with modern tracker technology achieves 1,150–1,400 kWh/kWp/year, depending on the location. For landowners, this means that a 10-hectare site can generate between 10 and 14 MWp of power, depending on the array configuration—and thus make a significant contribution to regional energy production. Many ground-mounted PV systems are now deliberately designed with higher row density.

| Mounting of the FFA | Space requirements | Typical applications | Source |

|---|---|---|---|

| South-facing, fixed (standard) | ~1.0 ha/MWp | Standard projects: 5–50 MWp | C.A.R.M.E.N. e.V., November 2025 |

| East-West, bifacial | 0.7–0.8 ha/MWp | Grid-friendly output profiles, large solar farms | Industry Data / ohana-invest.de, 2026 |

| Single-axis tracker (south-north) | 1.1–1.3 ha/MWp | Locations with high levels of direct sunlight | Fraunhofer ISE, July 2024 |

| Ground-mounted solar power systems with row trackers | 0.9–1.1 ha/MWp | Medium-sized orchards, higher yields per acre | Fraunhofer ISE, July 2024 |

| Sources: C.A.R.M.E.N. e.V. Position Paper 11/2025 · Fraunhofer ISE 07/2024 · ohana-invest.de 2026 | |||

Suitable sites under the Renewable Energy Act

Section 37(1)(2) of the Renewable Energy Act specifies which areas are eligible to participate in tenders. These include land converted from economic, military, or transportation use; the shoulder strips along highways and double-track railway lines (up to 500 m since Solar Package I of May 16, 2024); arable land located in disadvantaged areas; sealed surfaces; landfills; parking lots; and rewetted peatlands. The state opt-out clause under Section 37c of the EEG has been an opt-out since Solar Package I: If no state issues an exclusion regulation, sites in disadvantaged areas are eligible for EEG funding nationwide. As of March 2026, no state has made use of the opt-out option—not even in areas such as Baden-Württemberg, Bavaria, or North Rhine-Westphalia.

Minimum lot size and proximity to the power grid

Three factors determine the economic viability of a site. First, size: Open-field solar plants are rarely profitable on sites smaller than about 3 hectares, because the fixed costs for planning and grid connection per kWp are too high. Second, proximity to the grid: A medium-voltage substation located less than 3 km away keeps grid connection costs below €150,000 per feed-in point. Third, conservation status: Natura 2000 sites, FFH areas, and landscape conservation areas are effectively off-limits. A reputable project developer will reject any proposal that cannot be approved—this protects landowners from years of idle contracts.

What legal framework will apply to ground-mounted solar power in 2026?

Three sets of regulations govern the construction of ground-mounted photovoltaic systems. Since January 11, 2023, Section 35(1)(8)(b) of the German Building Code (BauGB) has granted preferential treatment to ground-mounted PV systems within a 200-meter strip along highways and double-track railways. The Renewable Energy Act (EEG) even extends this corridor to 500 meters under Section 37(1)(2)(c) (Solar Package I, May 16, 2024). For areas in disadvantaged regions, an opt-out for the federal states has been in effect since Solar Package I—currently, no federal state has issued an exclusion regulation. EEG support thus forms the economic backbone of ground-mounted photovoltaics in 2026.

Privileges under the German Building Code (BauGB): Section 35(1)(8)(b) and the 200-meter strip

Since the amendment to the German Building Code (BauGB) on January 11, 2023, ground-mounted photovoltaic systems within the 200-meter buffer zone along highways and double-track rail lines of the main network have been granted special status under land-use planning law. “Special status” means that the project is permitted without a separate zoning plan, provided that there are no conflicting public interests. This accelerates the approval process and reduces project development time by 6–12 months. The legally mandated buffer zone of 200 m is the BauGB standard; the eligible zone under the Renewable Energy Act extends as far as 500 m. Between these two values, ground-mounted PV systems are thus eligible for support but require a zoning plan.

EEG Subsidies: Section 37 of the EEG and the State Opening Clause

Section 37(1)(2) of the Renewable Energy Act defines which areas are eligible to participate in open-space tenders. In addition to privileged field margins, conversion areas, and sealed surfaces, this includes areas in disadvantaged regions—though subject to an 80-GW cap through 2030 under Section 37(4) of the EEG, which increases to 177.5 GW starting in 2031. As of November 30, 2025, according to the Federal Network Agency (BNetzA), 14.7 GW of open-space wind farms have been installed on agricultural land.

The state opt-out clause in Section 37c(2) of the EEG was changed from an opt-in to an opt-out provision with Solar Package I on May 16, 2024: Land in disadvantaged areas is eligible for EEG subsidies nationwide, unless the state actively excludes it. As of April 2026, no federal state has issued an exclusion regulation—neither in areas of Baden-Württemberg, Bavaria, or Saxony, nor in areas in northern Germany. EEG subsidies thus remain the most important revenue driver for project developers and, among others, for municipally-backed community energy projects.

Conservation requirements: 3 out of 5 biodiversity criteria are mandatory

Solar Package I has tightened the environmental and nature conservation requirements for ground-mounted PV systems. Under Section 37(1a) and Section 48(6) of the Renewable Energy Act (EEG), operators of new projects awarded through tenders must meet at least 3 of the 5 defined biodiversity criteria:

Extensive grassland management without pesticides or mineral fertilizers

Flower-rich borders within a specified area

Habitat structures such as deadwood, stone piles, and small bodies of water

Module coverage of less than 60% of the plot area

Minimum width of undeveloped buffer strips bordering adjacent properties

These requirements are a prerequisite for the tender and influence the calculation of the lease price. They protect nature and the landscape while also contributing to climate protection through solar power generation—a dual contribution to the environment and the energy transition.

How much will ground-mounted solar power systems cost in 2026?

The investment costs for ground-mounted photovoltaic systems larger than 10 MWp will range from €600 to €900 per kWp on a turnkey basis (solar modules, inverters, mounting structures, civil engineering, grid connection, and planning) in 2026. Ground-mounted systems between 1 and 10 MWp cost €700–1,000/kWp, while smaller ground-mounted PV systems under 1 MWp cost €900–1,100/kWp (Fraunhofer ISE / BSW Solar, Q1 2026). Fraunhofer ISE estimates the levelized cost of electricity at 4.1–5.0 ct/kWh in southern Germany and 5.7–6.9 ct/kWh in northern Germany. Module prices in 2025/26 will range between €0.09 and €0.15/Wp.

Capital expenditures by project size

Economies of scale are clearly evident in ground-mounted photovoltaic systems. The larger the ground-mounted PV system, the lower the price per installed kWp. Large ground-mounted PV systems can negotiate better terms for solar modules and mounting structures, spread planning costs across more megawatts, and benefit from more efficient logistics during installation. The cost structure for ground-mounted PV systems is divided into six categories: modules, inverters, mounting structures, civil engineering, grid connection, and planning. Investment costs differ significantly between traditional ground-mounted PV systems and elevated dual-use systems—the latter are typically 30–50% more expensive.

| FFA size class | Capital costs (€/kWp) | Breakdown by Modules / Wind Power / UK / Civil Engineering / Grid / Planning | Source |

|---|---|---|---|

| < 1 MWp | 900–1,100 | 30 / 10 / 15 / 15 / 15 / 15% | Fraunhofer ISE / BSW Solar, Q1 2026 |

| 1–10 MWp | 700–1,000 | 32 / 10 / 16 / 16 / 14 / 12% | Fraunhofer ISE / BSW Solar, Q1 2026 |

| > 10 MWp Sweet Spot | 600–900 | 35 / 10 / 17 / 17 / 12 / 9% | Fraunhofer ISE / BSW Solar, Q1 2026; Logic Energy project estimates for 2026 |

| Floating PV | 850–1,200 surcharge | +40% Subfloor / Floating system | Market Sources 2026 |

| Sources: Fraunhofer ISE / BSW Solar Price Monitor Q1 2026 · Fraunhofer ISE Levelized Cost of Electricity 07/2024 · Logic Energy Project Calculations 2026 · Benchmark average for turnkey projects ~€1,015/kWp (Fraunhofer ISE July 2024) | |||

Operating costs and insurance

In addition to the one-time installation costs, there are annual operating costs. In its latest market report, Fraunhofer ISE estimates these costs at €10–25 per kWp per year, or 1–2% of the total investment. These costs include technical management, insurance, property tax, lease payments, and monitoring.

Decommissioning reserves and security deposits

In addition to ongoing operating costs, a decommissioning reserve of typically €30,000–50,000 per MWp is required, which authorities demand as a bank guarantee for the end of the project. Anyone operating a 20 MWp plant should therefore budget for approximately €600,000–1,000,000 in decommissioning security—an important factor in the profitability calculation that is often missing from many online calculators.

Electricity Generation Costs Fraunhofer ISE

Levelized cost of electricity determines whether ground-mounted photovoltaic systems are economically viable even without subsidies. According to the Fraunhofer ISE study from July 2024, these costs range from 4.1 to 5.0 ct/kWh in southern Germany and from 5.7 to 6.9 ct/kWh in northern Germany. The difference stems from global radiation: Southern Germany reaches around 1,300 kWh/m²/year, while Northern Germany tends to reach 1,050 kWh/m²/year. These values for solar power from a ground-mounted PV system are significantly below the production costs of all fossil fuel alternatives and below the annual average on the electricity exchange. This explains the 2025 turning point toward PV systems in the open-field segment as PPA projects without feed-in tariffs. The open-field PV system thus becomes an independent producer.

How will electricity from ground-mounted solar power plants be compensated in 2026?

Solar power from ground-mounted PV systems with a capacity of 1 MWp or more is marketed in Germany through EEG tenders issued by the Federal Network Agency. Ground-mounted solar systems with bid prices such as the volume-weighted award price of 4.84 ct/kWh (BNetzA) as of July 1, 2025, set the market pace. The maximum value for the bidding date of March 1, 2026, is 5.79 ct/kWh. Smaller community energy projects between 1 and 6 MWp receive a fixed remuneration outside the tender process. A ground-mounted PV system with direct marketing as a corporate PPA will achieve 55–65 €/MWh in 2025/26 (LevelTen). Such ground-mounted solar plants form the backbone of the market.

BNetzA Tender Results 2025/2026

The Federal Network Agency conducts three auctions per year for Segment 1 (ground-mounted photovoltaic systems over 1 MWp). The auctioned volume for 2026 is 9,900 MW, in accordance with Section 28a of the Renewable Energy Sources Act (EEG). The award prices range from 4.66 to 5.00 ct/kWh; the maximum price was set at 5.79 ct/kWh for the bidding deadline of March 1, 2026—an increase that reflects higher financing costs and increased grid connection costs.

| Bidding deadline | Volume | Volume-weighted average | Oversubscription | Source |

|---|---|---|---|---|

| 01.03.2025 | 3,100 MW | 4.66 cents per kWh | approx. 180% | BNetzA / pv-magazine 03/2025 |

| 01.07.2025 | 2,850 MW | 4.84 cents per kWh | approx. 200% | BNetzA July 1, 2025 |

| 01.12.2025 | 2,328 MW (awarded: 2,341 MW) | ~5.00 cents/kWh | 225% 5,247 MW bids | BNetzA / photovoltaik.eu December 2025 |

| March 1, 2026 ( current) | approx. 3,200 MW | open, maximum value 5.79 ct/kWh | Open Publication: April 20–30, 2026 | BNetzA Decision 12/2025 |

| Sources: Federal Network Agency (BNetzA) – Closed tenders for Solar 1 · pv-magazine.de 03/2025 + 12/2025 · BNetzA maximum value set in 12/2025 | ||||

Fixed compensation outside the scope of the request for proposals

Community energy projects up to 6 MWp can be exempted from the tendering requirement under Section 22b of the Renewable Energy Act (EEG) and receive a fixed feed-in tariff of approximately 5.48 ct/kWh (as of 2026, BSW-Solar). This is an important option for regionally based cooperatives, municipalities, and smaller community projects—the bureaucracy of the bidding process is eliminated, though the remuneration tends to be slightly below the tender average. Citizens also benefit from local value creation (see Section 8). Open-space PV systems up to 1 MWp outside the tender process (Section 48(1a) EEG) also fall under this regime.

Corporate PPA Prices for 2025/2026

In addition to government subsidies, the market for corporate power purchase agreements (PPAs) has become well established. In this model, the solar park operator sells electricity directly to an industrial customer—usually under a 10- to 15-year contract. German market prices for solar PPAs ranged between €55 and €65/MWh in 2025 (LevelTen, maysunsolar). Many large investors today combine feed-in tariffs for the first few years with a repowering PPA in later years—or build entire ground-mounted photovoltaic plants from the outset as unsubsidized PPA projects.

Regulatory Outlook for 2027: CfD and Solar Package

With the draft bill dated February 27, 2026, the federal government plans to introduce production-based two-way contracts for difference (CfDs) for new installations of 100 kW or more. This represents a structural shift, as the revenue side will be more closely linked to the market value of solar power and clawback mechanisms will come into effect. The impact on solar park investors is explained in detail in the cluster article on the planned mandatory CfD requirement for solar park investors starting in 2027. The current maximum values and premium values for 2026 are also continuously updated there.

Do you own 3 hectares or more in Germany? Logic Energy will assess your land free of charge for eligibility for subsidies, proximity to the grid, and the permitting process. Request an open-field solar plant

Lease rates for ground-mounted solar farms: what landowners will receive per hectare in 2026

In 2026, landowners typically receive €2,500–4,500 per hectare per year for leasing their land, and up to €5,000 per hectare per year in prime locations (flaechenmakler.de, landverpachten.de). This is many times the average agricultural lease rate— which was around €375/ha/year in 2024/25 (Federal Statistical Office; Thünen Institute 2022: €274). The lease price is determined by location (prime strip, proximity to the grid), land size, and lease term.

Market range and prime locations

The range of lease rates follows clear rules. Prime locations under Section 35 of the German Building Code (BauGB)—that is, the 200-meter strip along a highway or railway—command the highest lease rates because there is no zoning plan risk and the project development time is short. Proximity to the grid drives up prices because it reduces the cost of grid connection. Conversion sites in eastern and central-eastern Germany, as well as locations in Brandenburg, Mecklenburg-Western Pomerania, and Saxony-Anhalt, showed particularly strong growth in 2024/25—a decisive factor for farmland owners considering an alternative to traditional agricultural use.

| Location / Land category | 2026 Lease Rate (€/ha/year) | Typical duration | Source |

|---|---|---|---|

| Standard Farmland Without Solar Panels (Agricultural) Comparison | approx. 375 | Ages 9–12 | Thünen Institute / Federal Statistical Office 2024/25 |

| Open space in a disadvantaged area | 2,500–3,500 | 20–30 years + option | flaechenmakler.de 2025/26 |

| Brownfield sites / Vacant lots | 3,000–4,500 | 25–30 years + option | landverpachten.de 2025/26 |

| Prime location (200-meter strip under Section 35 of the German Building Code) Premium | 4,000–5,000 | 30 years + extension | flaechenverpachten.de 2025/26 |

| Sealed surface (parking lot, landfill) | 2,000–3,000 | 20–30 years | Market Sources 2026 |

| Sources: Thünen Institute / Federal Statistical Office, Lease Price Index 2024/25 · flaechenmakler.de 2025/26 · landverpachten.de 2025/26 · flaechenverpachten.de 2025/26 | |||

Lease Agreement Clauses: The Five Most Important Points

A lease agreement for ground-mounted photovoltaic systems is not a standard form but a multi-page contract. Five clauses are particularly important:

Indexation (index clause): The lease payment must be indexed—usually linked to the consumer price index. Without indexation, the nominal lease payment loses about 40% of its real purchasing power over 30 years, assuming 2% inflation.

Term: The standard term is 20–25 years, plus an option to extend for an additional 10 years. Shorter terms prevent bank financing.

Demolition clause: The lessee is obligated to completely demolish the facility and restore the site to its original condition—including a bank guarantee or security deposit covering the entire term.

Land registry easement: A limited personal easement in favor of the financing bank is mandatory—without it, large-scale open-space facilities cannot obtain external financing.

Repowering clause: Allows the lessee to replace the solar modules with higher-output ones after 15–20 years to ensure the system remains up to date technologically.

Special Tax Provisions for Landowners

Leasing has tax implications that should be clarified before the contract is signed. The agricultural land status may be lost if the area is used exclusively for PV for more than 20 years. This affects inheritance and gift taxes because agricultural land status results in a significantly lower market value than that of a technical area. CAP premiums cease from the time the PV system is installed—for dual-use systems where agricultural activity continues, a portion of the premiums is retained. Income from the lease agreement is classified as income from renting and leasing under Section 21 of the Income Tax Act (EStG), no longer as income from agriculture and forestry. A brief consultation with a tax advisor costs €200–500 and can save you from five-figure surprises down the line.

How long does it take to obtain approval and connect to the grid for ground-mounted photovoltaic systems?

The preparation of a zoning plan typically takes 6–12 months (solaranlagen-portal.com). Including preliminary planning, public participation procedures, the award of the contract, and grid connection, a total development period of 2–4 years is realistic (Solar PG). Projects eligible for expedited approval under Section 35 of the German Building Code (BauGB) do not require a zoning plan and shorten the timeline by 6–9 months. Grid connection to the higher-level grid at 100 MW and 110 kV is regulated under Section 1(1) of the KraftNAV (as amended on December 23, 2025).

Legal Basis for Construction: Urban Land-Use Planning and Rural Areas

Ground-mounted photovoltaic systems require a building permit and are subject to urban land-use planning; a valid zoning plan is required if the systems are to be constructed in an out-of-town area. Specifically, this means that without a zoning plan, the system is generally not permitted in rural areas—unless it falls under a statutory exemption such as Section 35(1)(8) of the German Building Code (BauGB) (a 200-meter strip along a highway or railway) or is constructed on land already zoned for development (such as industrial or commercial zones). Urban land-use planning is the responsibility of local authorities and is thus the municipality’s central instrument for controlling development.

Zoning plan process: 6–12 months

For non-privileged ground-mounted photovoltaic systems, the municipality requires a project-specific zoning plan. The process involves several steps: early public participation, public review, consultation with relevant agencies, and a resolution by the municipal council to adopt the zoning plan. Concurrently, a nature conservation review, a preliminary environmental impact assessment, and an assessment under species protection laws are conducted.

The role of local governments in the permitting process

Municipalities with experience in solar parks can complete the zoning plan process in 6–8 months; for those new to the process, it typically takes 12 months or more. Logic Energy supports municipalities throughout this process with a comprehensive planning package that includes a preliminary review, selection of experts, and a public engagement format. This accelerates the process and significantly reduces the municipality’s risk costs.

Grid connection: Medium- and high-voltage, maturity assessment process

Grid connection will be the second critical path in 2026. Small and medium-sized ground-mounted PV systems (up to approx. 20 MWp) connect to the medium-voltage grid—the responsible distribution system operator is the point of contact here. Large-scale projects of 100 MW or more connect to the high-voltage or extra-high-voltage grid and fall under the scope of the Power Plant Grid Connection Ordinance (KraftNAV). The KraftNAV was fundamentally revised as of December 23, 2025: Large-scale battery storage systems are no longer subject to the regulation, and for new large-scale projects, a maturity assessment procedure based on the “first ready, first served” principle is expected to be introduced starting in April 2026. Details on the maturity levels and the new implementation deposit of €1,500/MW are covered in the cluster article on the KraftNAV amendment and the new 2026 maturity assessment procedure.

Regional conditions: Baden-Württemberg, Bavaria, North Rhine-Westphalia

The states implement the federal legal framework in different ways. In Baden-Württemberg, the state has set a target of 40 GW of solar PV by 2040 and significantly streamlines the process for PV installations in disadvantaged areas. Within the context of the Renewable Energy Act (EEG), Baden-Württemberg has taken an active role and granted grid connection priority to PV installations. Bavaria requires an in-depth EIA for open spaces larger than 20 ha and has a significant regional grid connection backlog—the Bavarian Ministry of Economic Affairs alone reports 25 GW of renewable energy grid connection applications. North Rhine-Westphalia prioritizes conversion and slag heap sites with special EEG subsidies. The exact conditions vary across the ministries’ individual position papers—for project calculations, this can quickly add up to a 3–9-month time difference. Landowners in Baden-Württemberg, Bavaria, and North Rhine-Westphalia also benefit from state advisory services regarding EEG support for PV systems.

Solar Farms as an Investment: Factors Driving Returns and Market Conditions

Institutional solar park investments typically yield an IRR of 5–8% per annum in 2026 (market range according to bne/trade press). The KfW 270 subsidy offers effective interest rates ranging from 3.25% to 10.78%, depending on credit rating, with terms of up to 30 years (KfW, 01/2026). For commercial investors, tax benefits include a 50% investment deduction (§ 7g EStG), a 40% special depreciation allowance, and a 30% declining balance depreciation, all of which can be combined until the end of 2027.

IRR Range and Market Delineation

The profitability of a ground-mounted photovoltaic system depends on six factors: site-specific global radiation, premium value or PPA price, investment costs per kWp, financing structure, OPEX discipline, and assumed project duration. According to bne data and trade press benchmarks, the market range for institutional solar park investments is between 5% and 8% p.a. IRR—based on conservative, unleveraged calculations. Detailed return scenarios for businesses and investors—including battery storage co-location and PPA comparisons—are provided in the 2026 Return Guide on Return Drivers for Solar Parks. An overview of the return opportunities of direct PV investments as an asset class can be found on the Investment Pillar.

The figures listed here are market benchmarks for institutional solar parks. Specific returns and tax terms for Logic Energy’s inverter investment model, including a full investment disclaimer, can be found on the Photovoltaic Investment 2026 page.

Financing: KfW 270 and debt capital structures

The KfW 270 is the most important financing instrument for solar parks. Current effective interest rates range from 3.25% to 10.78% across 9 pricing tiers (as of KfW, 01/2026). The loan term is up to 30 years, with up to 5 grace years available. Banks typically require 20–30% equity. The maximum loan amount is €150 million per project. Applications are submitted through the applicant’s primary bank prior to the start of construction. At the same time, the ECB deposit rate, currently at 2.00% (unchanged since June 11, 2025), shapes refinancing conditions in the market.

Investment deduction (IAB) pursuant to Section 7g(1) of the Income Tax Act

Commercial investors in ground-mounted photovoltaic systems take advantage of the investment deduction under Section 7g of the German Income Tax Act (EStG). This allows for an upfront deduction of up to 50% of the planned acquisition costs in the year prior to the investment, limited to a €200,000 reduction in taxable income. The investment deduction acts like an interest-free loan from the tax office and significantly reduces the tax burden in the planning year—provided the investment is intended and reported on the previous year’s tax return.

Special depreciation under Section 7g(5) of the Income Tax Act: 40% over the first 5 years

The special depreciation under Section 7g(5) of the German Income Tax Act (EStG) allows for an additional 40% depreciation spread over the first five years following commissioning (Growth Opportunities Act 2024). Unlike straight-line depreciation, the special depreciation can be freely allocated over the five-year period—this provides flexibility for tax optimization depending on the company’s profit situation.

Investment Incentive: 30% declining balance depreciation through the end of 2027

In addition to IAB and special depreciation, the new 30% declining-balance depreciation rate under the 2025 Immediate Investment Program applies, effective through December 31, 2027. These three instruments can be combined. In the first year of use, this means that approximately 77% of the acquisition costs are tax-deductible—a detailed calculation is provided in the article “Saving on Photovoltaic Taxes in 2026.”

Local Economic Value Creation for Municipalities and Residents

Solar farms also provide reliable revenue for the host communities. Since 2021, business tax has been allocated in a 90/10 ratio pursuant to Section 29(1)(2) of the Business Tax Act (GewStG)—90% goes to the host communities. In addition, pursuant to Section 6 of the Renewable Energy Act (EEG), municipalities receive a financial share of 0.2 cents per kWh. A 50-MWp park with an annual output of 55 GWh generates approximately €110,000 in annual revenue, in addition to the trade tax. Local residents benefit from local economic value creation, potential community participation models, and regionally discounted electricity rates—this is a strong argument in the zoning plan process and a concrete contribution to the local energy transition.

Outlook: AgNes and feed-in tariffs

Starting in 2026/27, the AgNes reform will introduce an additional factor into the profitability calculation. In February 2026, the Federal Network Agency published guidelines on the construction cost subsidy for feed-in (BKZ-E), which will result in additional costs per kW for new feed-in operators. The Regulatory Cluster discusses in detail how the AgNes reform will affect the economic viability of ground-mounted investments.

Biodiversity: How Solar Farms Can Create Habitats for Wildlife

The bne field study “Biodiversity in Solar Parks” from March 2025 identified over 350 plant species, 34 butterfly species, and 30 grasshopper species across 30 solar parks surveyed—a measurable contribution to biodiversity compared to intensively farmed land, thanks to extensive management practices that avoid the use of pesticides and mineral fertilizers. The study received third place at the European Solar Sustainability Award in December 2025 (SolarPower Europe).

The 2025 ESD Field Study: Impacts on Nature and the Environment

In 2024/2025, the German Renewable Energy Federation (bne) conducted the most comprehensive field study to date on biodiversity in German solar parks. The study examined 30 parks in five federal states over two growing seasons. The result: With extensive maintenance, the areas beneath and between the solar modules develop into a diverse habitat. Skylarks and sand lizards regularly appear as indicator species, while wild bee populations and ground-nesting birds benefit from the pesticide- and fertilizer-free areas. Larger animal species such as hares and deer are also regularly documented in the parks. The positive impacts on nature, the landscape, and the environment are documented in peer-reviewed studies—and dispel the misconception that solar parks are barren landscapes.

Good professional practice and minimum criteria

This level of biodiversity is not a matter of chance, but the result of specific management measures. Solar Package I has established a minimum standard for nature conservation in Section 37(1a) and Section 48(6) of the Renewable Energy Act (EEG)—3 out of 5 defined measures are mandatory:

Avoiding the use of pesticides in land management

Flower-rich borders within a specified area

Habitat structures such as deadwood, stone piles, and small bodies of water

Module coverage of less than 60% of the plot area

Minimum width of undeveloped buffer strips adjacent to neighboring properties

Reputable project developers go above and beyond the minimum requirements—because this increases acceptance among residents and in the local community and unlocks lease premium increases for environmental certifications. Anyone leasing land should explicitly include these points in the contract. This allows for positive management of impacts on animal and plant species, and open-space photovoltaics becomes an opportunity rather than a source of conflict for nature and the landscape.

Special types of ground-mounted photovoltaic systems: floating, parking lot, peatland

In addition to traditional ground-mounted photovoltaic systems, there are several specialized types with specific capabilities and requirements. Floating PV systems are installed on bodies of water. The development of sealed surfaces for parking lot PV is a growing segment. Re-wetlanded peatlands offer a dual contribution to climate protection. For dual-use applications combining agriculture and solar power, please refer to the sub-pillar page onagri-photovoltaics.

Overview of Special Uses

Floating PV is well-suited for disused quarry ponds and reservoirs. Several pilot projects exist in Germany, but the market remains small. Parking lot PV covers existing parking areas—ideal for businesses, wholesalers, and municipalities because it also provides weather protection for vehicles. The use of sealed surfaces is subsidized under Section 37 of the Renewable Energy Act (EEG). Moor PV on rewetted peatlands reduces GHG emissions from the soil while simultaneously producing solar power—a dual strategy for climate protection and the energy transition. Agri-PV systems also technically belong to the family of ground-mounted solar systems, but are treated as a separate sub-pillar due to their dual agricultural use. All of the variants mentioned are essentially ground-mounted photovoltaic systems with specific site characteristics and contribute to the expansion of renewable energy generation.

By 2026, ground-mounted solar farms will be the dominant form of PV expansion in Germany. For landowners, this means lease payments of €2,500–5,000 per hectare per year—eight times the standard agricultural lease rate. For investors, a market is opening up with a 5–8% IRR and a limited time window before the CfD requirement takes effect in 2027. For municipalities and citizens, solar parks bring a 0.2 ct/kWh share plus 90% of the business tax to the local area. The legal framework is favorable: 200-meter exemption under Section 35 of the German Building Code (BauGB), state opt-outs under Section 37c of the Renewable Energy Act (EEG), and a maximum rate of 5.79 ct/kWh for the March 2026 deadline. With battery storage integration and grid-friendly direct marketing, modern ground-mounted photovoltaic systems tap into additional revenue streams beyond traditional feed-in tariffs—an important contribution to the energy transition and climate protection.

The next step is always a free initial assessment. We evaluate sites and investment inquiries within 14 days and provide specific figures: lease terms, project size, and implementation timeline. An overview of all Logic Energy photovoltaic systems can be found on the parent page.

Do you have open land starting at 3 hectares to offer, or would you like to invest starting at €100,000? Request information on open-field installations (landowners)

Inquire as an investor · Process: Invest in German solar parks starting at 100,000 EUR — Investment process

Do you own unused land and want to lease or sell it long-term? With ground-mounted solar panels, you can turn idle or low-yield land into a predictable source of income!

Your benefits:

Long-term, predictable lease income or solar power revenue

If you lease the property, you remain the owner

No more management costs

Increase in the value of the property

Ecological enhancement

No soil sealing

Potential for dual use

Contribution to the energy transition

What types of land are suitable?

Generally suitable:

Farmland with low productivity (marginal soils)

Grassland with poor soil quality

Brownfield sites (former military, commercial, or industrial sites)

Areas along highways and railroad tracks (200-meter-wide strips)

Wasteland, gravel pits, landfills (after remediation)

Not suitable:

Nature reserves

Sites designated as historic landmarks

Areas with heavy shade

Areas in floodplains (without special measures)

For landowners:

DO YOU HAVE LARGE PARCELS OF LAND TO SELL OR LEASE?

FOR INVESTORS:

INDUSTRIAL SOLAR PARKS AS AN INVESTMENT

Are you interested in investing in large-scale solar projects? With our open-field model, you can invest in professionally developed solar parks ranging from 30 MWp to utility-scale projects exceeding 250 MWp. We manage the entire value chain—from project development, site acquisition, and permitting to EPC and long-term operations.

What you get:

Ready-to-build projects with guaranteed land availability

Full-scale project development: site analysis, permitting process, grid connection, financing structure

EPC Services (Engineering, Procurement, Construction): We build your turnkey facility to the highest quality standards

Long-term operation (O&M): 20–40 years of professional management, maintenance, insurance, and monitoring

Investment in inverters starting at €100,000 or acquisition of entire solar farms

Personal liability of the owner (sole proprietorship) – Contract with mediplan Helm e.K.

Financing assistance is available through our bank

Important Note: The information on this page is intended solely to provide general information about ground-mounted solar parks as an investment opportunity. It does not constitute investment, tax, or legal advice and is not a substitute for individual consultation with a licensed professional advisor. Return figures are based on empirical data and portfolio information from the Helm Group and are not a guarantee of future results. Tax planning options such as the investment deduction (IAB) under Section 7g of the German Income Tax Act (EStG) are subject to individual requirements—please consult your tax advisor regarding this matter. For your personal investment decision, please consult a licensed financial or tax advisor. All information is provided without warranty. As of April 2026.

FAQ

-

In 2026, market-rate lease payments for ground-mounted photovoltaic systems will range between €2,500 and €4,500 per hectare per year, and up to €5,000 per hectare per year in prime locations as defined by Section 35 of the German Building Code (BauGB). This is many times higher than the average agricultural lease payment of approximately €375 per hectare per year (Thünen Institute). Index clauses, term, and land registry easements have a greater impact on the effective value than the nominal interest rate.

-

Modern south-facing ground-mounted photovoltaic systems require approximately 1.0 ha per MWp (C.A.R.M.E.N. e.V., 11/2025). With bifacial east-west trackers, 0.7–0.8 ha/MWp is possible. An economically viable minimum size starts at 3–4 MWp on 4–5 hectares. For dual-use systems, up to 85 percent of the land can continue to be used for agriculture (see agri-photovoltaics).

-

Roadside strips up to 500 meters along highways and double-track railway lines are eligible for EEG subsidies (since Solar Package I, May 16, 2024), conversion areas, farmland in disadvantaged areas (up to the 80-GW cap in 2030), sealed surfaces, landfills, parking lots, and rewetted peatlands. The state opt-out clause under Section 37c of the EEG is an opt-out provision—to date, no state has opted out. EEG subsidies therefore currently apply nationwide without restriction.

-

Since January 11, 2023, Section 35(1)(8)(b) of the German Building Code (BauGB) has granted preferential treatment to ground-mounted solar installations within a 200-meter strip along highways and double-track railways. Within this corridor, the project is permitted without a separate zoning plan, provided that there are no public interests that would preclude it. This accelerates the approval process by 6–12 months compared to non-privileged locations.

-

For projects over 10 MWp, turnkey investment costs range from €600 to €750 per kWp; for projects between 1 and 10 MWp, they range from €750 to €900 per kWp; and for projects under 1 MWp, they range from €900 to €1,100 per kWp (market sources / Fraunhofer ISE, 2024/2026). Fraunhofer ISE estimates the levelized cost of electricity at 4.1–5.0 ct/kWh in southern Germany and 5.7–6.9 ct/kWh in northern Germany.

-

According to bne data and industry press benchmarks, the market range for institutional solar park investments is 5–8 percent per annum IRR (unleveraged, conservative). The "Photovoltaic Investment 2026" investment page explains specific scenarios with and without battery storage, as well as Logic Energy’s specific inverter investment.

-

For pure arable or grassland areas with low agricultural profitability, traditional ground-mounted systems are usually more economical—offering higher electricity yield per hectare and lower CAPEX of €600–750/kWp for projects of 10 MWp or more. For specialty crops, livestock pastures, or areas with high agricultural yield potential, dual-use agri-photovoltaics (CAPEX €900–1,500/kWp)is anoption worth considering, as up to 85% of the land remains usable for agriculture. The decision depends on eligibility for CAP subsidies and the land’s yield potential.

References

BauGB, as amended on January 11, 2023 — Section 35(1)(8)(b) (200-meter exemption)

Federal Law Gazette 2025 I No. 51 — Solar Peak Act, effective February 25, 2025

BNetzA — Solar 1 Tenders, Bid Deadlines: March 1, 2025 / July 1, 2025 / December 1, 2025 / March 1, 2026 (Maximum Price: 5.79 ct/kWh)

bne (German Association for New Energy) — Press Release: "Solar Parks Benefit Biodiversity," March 2025

C.A.R.M.E.N. e.V. — Position Paper, November 2025

Renewable Energy Act — in particular Section 37(1)(2), Section 37(1a), Section 37c, and Section 48(6)

EStG — Sections 7g(1), 7g(5), and 7(2) (2025 Immediate Investment Program)

Fraunhofer ISE — Study on Levelized Cost of Electricity, July 2024; Current Facts on Photovoltaics, December 2025

KfW — Program 270, as of January 2026

KraftNAV — as of December 23, 2025

Thünen Institute / Federal Statistical Office — Lease Price Trends, 2024/25